Reverse Mortgages In Phoenix: What Seniors and Their Kids Need to Know

If you’re helping a senior, or you’re the one thinking about retirement, the topic of reverse mortgages in Phoenix tends to come up at the kitchen table sooner or later. The problem is that most people only know the rumors, or what they saw in a TV ad, and that isn’t enough to make a good decision.

In this post, I’m going to walk you through what I learned in a sit-down with reverse mortgage specialist Kathy Burns, including how the purchase program works, why the line of credit is different than a HELOC, what happens to heirs, and the red flags I want you watching for.

Meet Kathy Burns, the reverse mortgage specialist I trust

I’m Bob Hertzog, “Your Real Estate Dad.” I spend a lot of my time helping Phoenix senior homeowners, their caregivers, and adult kids work through tough housing decisions, downsizing, rightsizing, or figuring out how mom or dad can stay put without getting squeezed every month.

Because reverse mortgages come up more and more, I brought in someone who lives and breathes this stuff: Kathy Burns, a reverse mortgage specialist and loan officer with Cross Country Mortgage. She was referred to me by my lender partner, Lizy Hoeffer, and the biggest thing I noticed right away is that Kathy teaches first. No pressure, no “one-size-fits-all” pitch.

If you want to talk with Kathy directly, here’s her number: 818-309-8083, or you can email her at Kathy.Burns@ccm.com.

What a reverse mortgage actually is (and what it’s not)

A reverse mortgage is a way to take home equity and turn it into a financial resource, without adding a required monthly mortgage payment. Kathy explained it as using your home equity alongside other retirement assets (like an IRA or 401(k)), instead of treating equity like “dead money” that you can’t touch.

Most of what we discussed focused on the FHA program called a HECM, which stands for Home Equity Conversion Mortgage. The reverse mortgage program has been around since the late 1980s, but it’s had a lot of updates over the years, mostly aimed at consumer protection.

Here are a few “plain English” points that clear up a lot of confusion:

- Primary residence only. This is for the home you live in, not a second home, Airbnb, or investment.

- You keep ownership and title. The lender does not “take your house.” It’s a lien, just like a traditional mortgage.

- The money is tax-free cash. The proceeds are loan funds, not income, so they’re not taxable just because you received them.

That tax piece matters more than people realize, especially when families are trying to create monthly breathing room without triggering extra tax problems.

No required mortgage payment, but you still have responsibilities

The biggest appeal is simple: with a reverse mortgage, there’s no mandatory monthly mortgage payments. Repayment is generally deferred until a “maturity event,” meaning the borrower permanently leaves the home (selling, moving out long-term, or passing away).

That said, the homeowner still has to handle the same basic obligations any homeowner has:

- Property taxes

- Homeowners insurance

- Home maintenance

If you’re not sure what taxes look like where your parents live (or where you might buy next), I wrote a detailed guide on Phoenix property tax rates and savings because those costs can sneak up on people, especially after retirement.

Here’s the trade-off Kathy emphasized: you gain monthly payment relief, but the loan balance grows over time because interest gets added to the balance (this is what lenders call negative amortization). Real estate often appreciates over the long run, which can help offset that growth, but the growing balance is still part of the deal.

Why Kathy sees reverse mortgages in Phoenix as safer than a HELOC for seniors

A lot of people lump HECM reverse mortgages and HELOCs together because both involve equity. The difference shows up when life gets messy.

During the 2007 to 2009 crash, many homeowners in Maricopa County watched their HELOCs get frozen or reduced. That’s scary for anyone, but it’s especially risky for retirees who depend on that line for emergencies or income.

With a reverse mortgage line of credit, Kathy explained two safety features that stand out:

- It can’t be reduced, called, or canceled because the market drops.

- It has non-recourse protection, meaning if the loan balance ever ends up higher than the home’s value, FHA covers the shortfall. The borrower (or heirs) aren’t personally on the hook for the difference.

If the housing market takes a hit, the reverse mortgage line of credit doesn’t get “pulled back” the way some HELOCs can.

That one sentence is a big reason this product keeps coming up in retirement planning conversations.

Who qualifies for reverse mortgages in Phoenix, and what lenders look at

For the standard FHA-approved HECM program, the minimum qualifying age is 62 or older. Kathy also noted that for higher-value homes (above the HECM limits), there are jumbo reverse mortgage options, and some of those start at age 55.

A few other practical qualifiers for a reverse mortgage loan:

- Primary residence rules: You must live in the home most of the year (Kathy described it as 51 percent).

- Income review: The lender checks for enough income to keep up with taxes, insurance, and property upkeep.

- Credit score isn’t required for the FHA program, but they do review a 24-month payment history.

What if one spouse is under 62?

This is a common scenario. One spouse meets the age requirement and the other doesn’t.

Kathy explained that the program has non-borrowing spouse protections, so the younger spouse can still stay in the home for life. The catch is that the loan amount is based on the younger spouse’s age, so the available proceeds can be lower.

The reverse mortgage purchase program: buy a home without a monthly mortgage payment

This is the part many families don’t know exists.

With the purchase program, which requires a home appraisal, you use a reverse mortgage loan to buy a home, and you still don’t have a required monthly mortgage payment. It’s often compared to an all-cash purchase because the monthly payment stress goes away, but you may not have to drain every dollar of cash to get it done.

Kathy’s rule of thumb was that buyers usually bring roughly 65 percent down, and the reverse mortgage covers about 35 percent (much different than a typical 20 percent down conventional loan).

Here’s the example she gave, in a simple table.

| Item | Amount |

|---|---|

| Home purchase price | $560,000 |

| Total cost with FHA insurance + closing costs | $581,000 |

| Reverse mortgage amount | $230,000 |

| Cash needed (down payment) | $351,000 |

The takeaway is the “buying power” effect: someone with about $375,000 cash could use a reverse mortgage purchase and buy a $560,000 one-story home, with a little cash left over.

In my world, this is often a downsizing move: selling a two-story that’s hard on the knees, then buying something easier. I see it in The Sheaborhood (85028), the Biltmore area (85016), and Arcadia (85018) all the time. If you’re considering that kind of lifestyle shift, my living in Biltmore Phoenix 85016 guide can help you picture what day-to-day life looks like in that area.

The refinance program: pay off a mortgage, create cash flow, or plan ahead

On the refinance side, a reverse mortgage can be used to eliminate an existing mortgage payment, which is one of the most common reasons people do it.

Kathy gave a simple example: if someone retires with a $2,000 monthly mortgage payment, and the reverse mortgage pays it off, that’s $2,000 a month of cash flow that shows up immediately.

The 60 percent first-year rule (and why it exists)

This is important. For a refinance, HUD’s loan limits in the HECM program restrict the lump sum you can access in the first year. Kathy described it as 60 percent in year one, then in month 13 the remaining amount becomes fully available.

That rule doesn’t apply the same way on a reverse mortgage purchase, because the purchase is a full draw to complete the purchase transaction.

Two planning examples Kathy shared

- Second home goal: Kathy described a homeowner using a reverse mortgage refinance to establish a line of credit from their current home, letting it grow, then using it later as a large down payment on a retirement cabin or condo.

- Assisted living deposit: Another example involved a 76-year-old homeowner using the maximum first-year amount available (after costs) to put down a deposit and secure a spot, then selling the original home later to finish the move.

Both examples had the same theme: use equity to reduce stress and create options for retirement planning, without adding a required monthly mortgage payment.

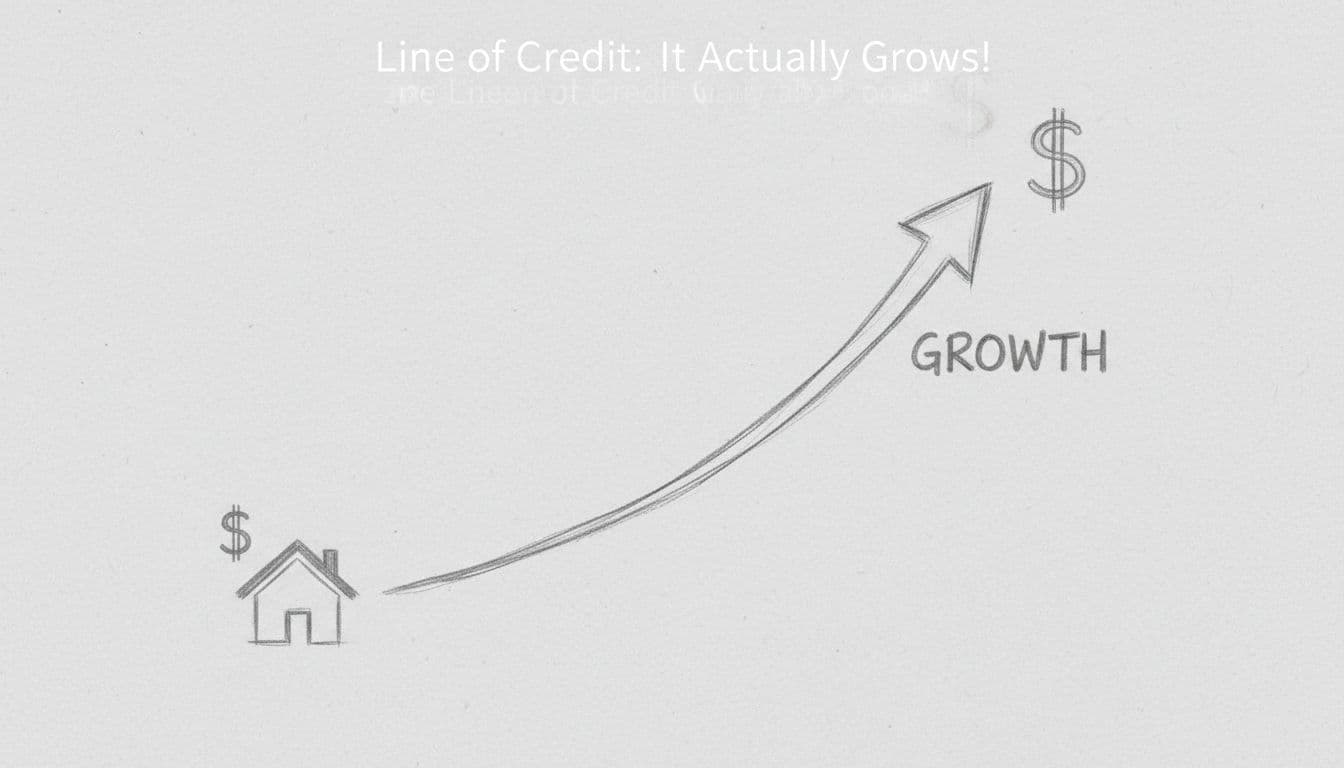

The reverse mortgage line of credit that grows over time

This feature surprises people, even smart ones.

Kathy explained that the reverse mortgage line of credit has two unusual traits:

- It can’t be frozen or reduced, even if home values drop in Maricopa County.

- The available line of credit grows at the same rate being charged on the loan balance, and it grows with compounded growth.

So, if someone had $100,000 available, and the growth rate was 7.24 percent, the available line could grow to roughly $107,000 after year one, then continue compounding after that, providing financial flexibility.

Kathy also pointed out that the line of credit guarantee can be well above FDIC insurance limits that people worry about with bank accounts. Plus, the funds you draw are still loan proceeds, so they remain tax-free.

What happens when the borrower leaves, and what heirs need to know

This is the question I get from almost every adult child: “Am I stuck with the debt?”

Kathy’s answer was clear: no, the debt isn’t transferred to heirs personally. The house is the collateral, and because of the non-recourse feature, if the loan ever ends up upside down, FHA covers the shortfall.

When a maturity event happens (the last borrower moves out long-term or passes away), heirs typically have options:

- Sell the home and use the proceeds to pay off the reverse mortgage loan (most common)

- Refinance into a traditional mortgage and keep the home

- Pay it off with other assets (life insurance, portfolio funds, etc.)

Kathy said the normal time frame starts with six months, and it can be extended up to one year (with two three-month extensions), as long as the heirs are communicating and the home is listed at a fair market value.

One more detail that matters: if a borrower like many Arizona seniors moves into a nursing home and is out of the house for 12 consecutive months, the loan becomes due, since the home is no longer the primary residence.

Myths, costs, and interest rates, in plain language

Reverse mortgages still have old myths attached to them. Reverse mortgage counseling is a requirement that helps clear them up, and Kathy addressed the big ones head-on:

- Myth: The bank owns the home. False. The homeowner stays on title.

- Myth: You can lose the house any time. Also false, as long as taxes, insurance, and upkeep stay current.

- Myth: It’s only for people in trouble. That used to be more common, but now many families use it as part of retirement planning.

- Myth: It ruins inheritance. Heirs can still keep the home if they want, they just have to pay off the loan like any other mortgage.

On cost, Kathy acknowledged the upfront costs can be higher, mainly due to FHA mortgage insurance, which helps fund the HUD-approved protections (non-recourse protection and the guaranteed line of credit).

Fixed vs. adjustable

Kathy explained that reverse mortgages can be fixed or adjustable (with proprietary reverse mortgage options available for high-value homes), but most borrowers choose adjustable because it supports flexibility (line of credit, monthly draws). Fixed-rate reverse mortgages usually require a full lump-sum draw upfront, which often doesn’t fit how retirees want to use the money.

Adjustable programs also have caps, including a lifetime cap on how high the rate can go. In addition, Kathy said reverse mortgages can be refinanced later if rates drop, similar to traditional mortgages.

Red flags and scam avoidance (Dad Talk)

Seniors and their kids are getting hit from every direction right now, and reverse mortgage marketing is part of that.

Here are the two red flags I want you watching for:

First, be cautious with unsolicited calls and “call this toll-free number for info” ads. Sometimes those are lead collectors for mortgage lenders, not the lender you’ll actually work with, and your information can get sold.

Second, watch for anyone pushing you to take more money than you need. Kathy’s point was simple: good loan design often means using only what you need, so interest doesn’t pile up faster than it has to.

In real life, the best version of this process includes the family and the advisors. As a loan officer, Kathy often talks with a client’s financial planner, CPA, or attorney because it’s usually the last big financial decision someone makes.

Reverse mortgages also aren’t for everyone. Sometimes a traditional mortgage, or even something like a bridge loan, fits better. I’ve seen that firsthand.

If you want to browse Phoenix downsizing options, you can start with my Phoenix home search. If you’re trying to figure out whether selling makes sense first, my home value estimate tool is a good starting point.

Conclusion

If you’re a senior homeowner weighing a reverse mortgage for yourself or a parent, you don’t have to rush it. The best outcomes come from understanding the trade-offs of tapping your home equity, then matching the program to the real goal in your retirement planning (monthly relief, downsizing, future care, or just peace of mind). If you want help thinking it through, I’m here, and Kathy is a solid, patient resource too. Above all, protect your family by sticking with referrals and clear education, not random phone calls and internet noise.